[Updated on January 21, 2023 with updated screenshots from H&R Block software for 2022 tax filing.]

When mutual funds and/or ETFs that invest in foreign countries receive dividends or interest, they have to pay taxes to those countries. These mutual funds and/or ETFs report to your broker after the end of the year how much they paid in foreign taxes on your behalf.

When you invest in these mutual funds and/or ETFs outside a tax-advantaged account, your broker will report to you the total foreign taxes you paid through all your funds and/or ETFs. The IRS allows a tax credit for the taxes you paid indirectly to foreign countries.

Form 1116

The foreign taxes paid is reported in Box 7 on the 1099-DIV form you receive from your broker. It’s easy to handle when the total foreign taxes paid from all your 1099-DIV forms is no more than a certain amount — $300 for single and $600 for married filing jointly. You enter the 1099-DIV forms into your tax software and the software will automatically put the total on your tax form (Schedule 3, Line 1).

When your total foreign taxes paid from all your 1099-DIV forms are over the $300/$600 threshold, you’ll need to include Form 1116 in your tax return. I’ll show you how to do this in H&R Block software.

If you use other tax software, please read:

Use H&R Block Download

The following screenshots came from H&R Block downloaded software. The downloaded software is both less expensive and more powerful than H&R Block’s online software.

If you haven’t paid for your H&R Block Online filing yet, consider buying H&R Block download software from Amazon, Walmart, Newegg, and many other places. If you’re already too far in entering your data into H&R Block Online, make this your last year of using H&R Block Online. Switch over to H&R Block download software next year.

I’ll use the same example:

You received a 1099-DIV from your broker. Box 7 “Foreign Tax Paid” on the 1099-DIV shows $700. 100% of this $700 came from a mutual fund or ETF. You only have this one 1099-DIV that has a number in Box 7.

1099-DIV Entries

If you import your 1099-DIV forms, double-check the import to make sure all the numbers match your downloaded copies. If you’re entering the 1099-DIV forms manually, type the numbers as shown on your forms.

H&R Block doesn’t say anything about the foreign tax paid or needing a Form 1116 after you enter the 1099-DIV forms. Just continue with your other entries.

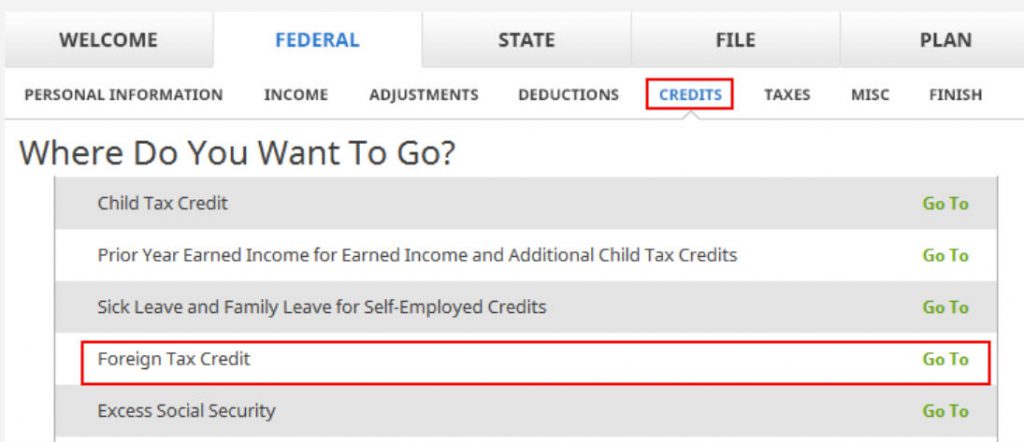

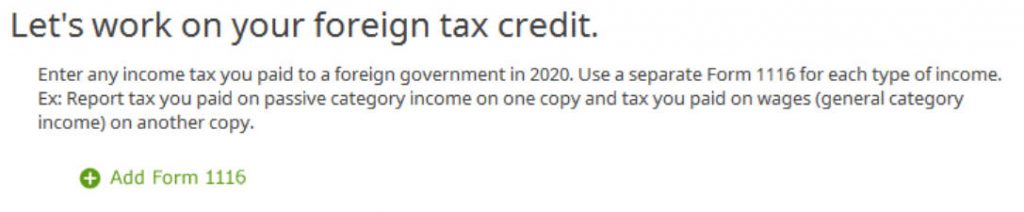

Foreign Tax Credit

Foreign Tax Credit comes up much later in the Credits section under Foreign Tax Credit.

Click on “Add Form 1116.”

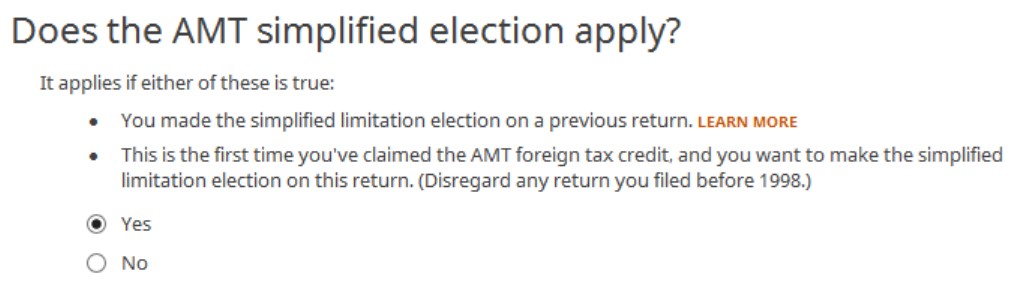

AMT Simplified Election

If this is the first year you’re claiming the Foreign Tax Credit, H&R Block software asks upfront about the simplified election. Select “Yes” for the simplified election.

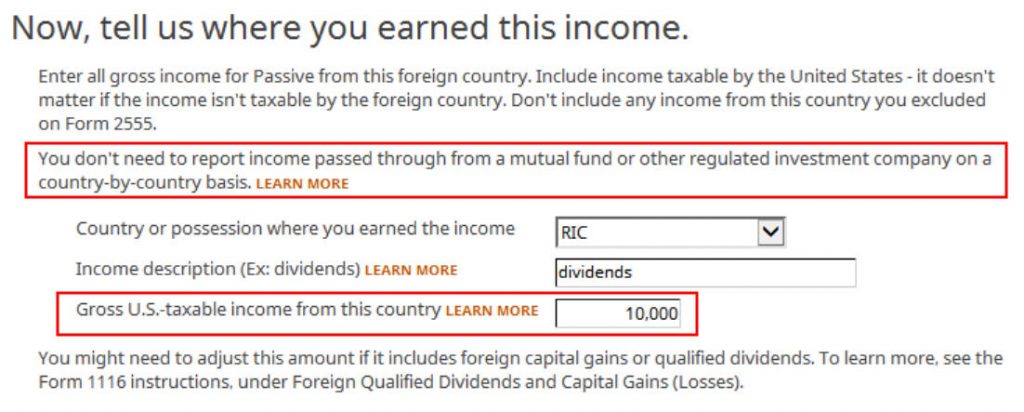

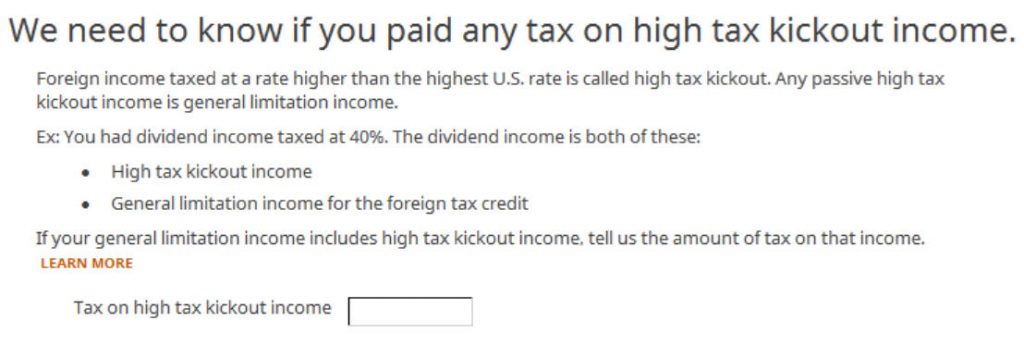

Foreign-Source Income

Dividend income falls under “passive income.”

The “learn more” popup says you should choose “RIC” as the country when your foreign income came through mutual funds and/or ETFs. “RIC” is the last item in the country dropdown.

You get the foreign income from the supplemental information in your 1099 package from your broker. If you have multiple 1099-DIV forms that reported foreign tax paid in Box 7, you’ll have to add up the foreign income numbers from the respective supplemental information.

Don’t overlook the small note under the gross income input. It says you might need to adjust the amount if it includes foreign capital gains or qualified dividends. When you’re reporting foreign taxes paid from mutual funds and ETFs, the income sure does include qualified dividends. H&R Block doesn’t do the adjustment for you. It asks you to read the IRS instructions, learn how to adjust, and report the adjusted income here. That’s lazy.

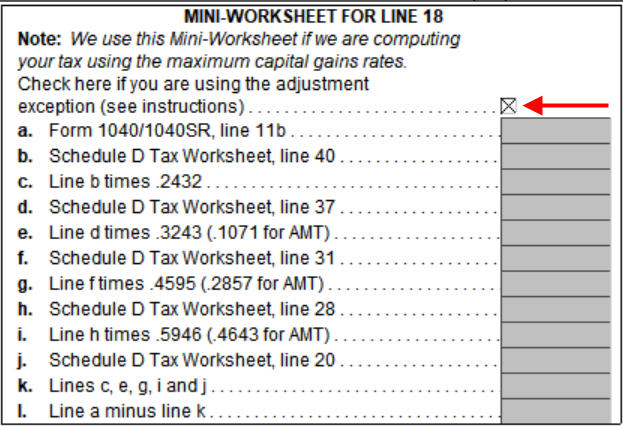

Adjustment Exception

Fortunately, many people qualify for an adjustment exception. From the IRS Form 1116 Instructions:

You qualify for the adjustment exception if you meet both of the following requirements.

1. Line 5 of the Qualified Dividends and Capital Gain Tax Worksheet doesn’t exceed:

a. $340,100 if married filing jointly or qualifying widow(er),

b. $170,050 if married filing separately,

c. $170,050 if single, or

d. $170,050 if head of household.2. The amount of your foreign source capital gain distributions, plus the amount of your foreign source qualified dividends, is less than $20,000.

The dollar amounts in the first requirement correspond to the top of the 24% bracket. You are spared from figuring out how to adjust if your taxable income minus your qualified dividends and long-term capital gains isn’t in the 32% tax bracket or above, and your foreign source capital gain distributions and qualified dividends aren’t $20,000 or more.

If you’re eligible for the adjustment exception and you decide to take the easy route of not adjusting your foreign-source income, you need to claim a corresponding adjustment exception on your total income.

Click on Forms on the top right. Open Form 1116. Scroll down and find Mini-Worksheet for Line 18 just above Line 18. Check the box for using the adjustment exception.

Close the form and return to the interview.

If you don’t qualify for the adjustment exception, good luck learning how to adjust from the Form 1116 instructions. You’re better off switching to TurboTax, which does the adjustment for you when you need it.

We leave this blank because we don’t have any interest expenses.

We leave this blank because we don’t have any other deductions either.

We don’t have any direct expenses either.

We have no losses to adjust.

Yes, our 1099-DIV was reported in U.S. dollars.

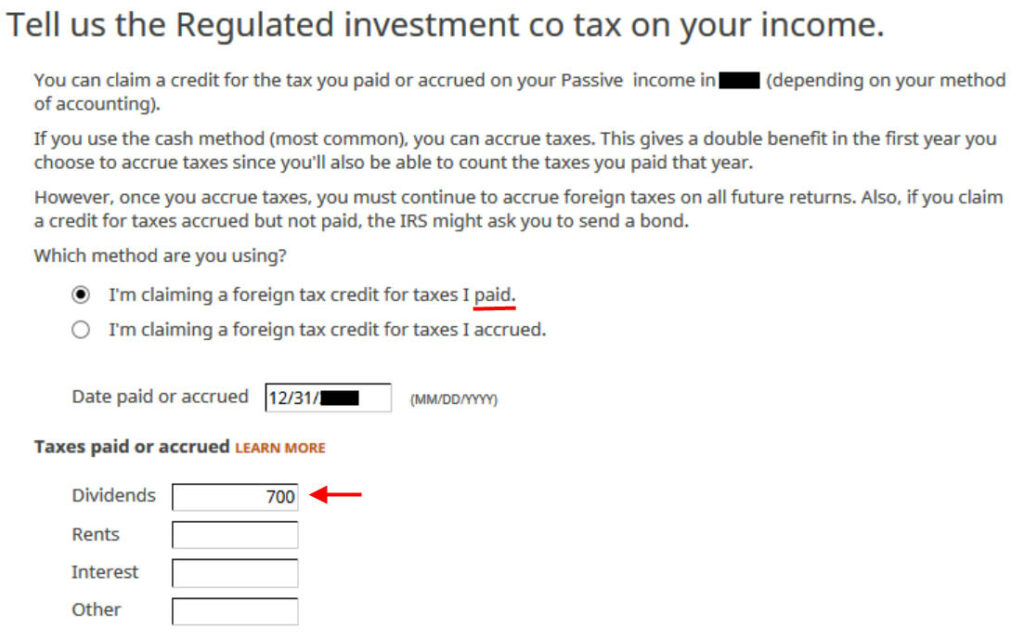

Foreign Taxes

I chose the simpler “paid” method. Enter the end of the year as the date paid. Enter the total foreign tax paid into the Dividends box.

If you have multiple 1099-DIV forms that reported foreign tax paid in Box 7, you’ll have to add up those numbers yourself. I wish the software did the math and auto-populated this field.

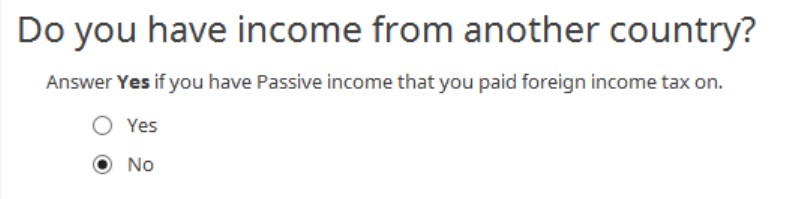

All our foreign taxes paid were through mutual funds and ETFs. RIC is the only country to use. We don’t have foreign income from any other countries.

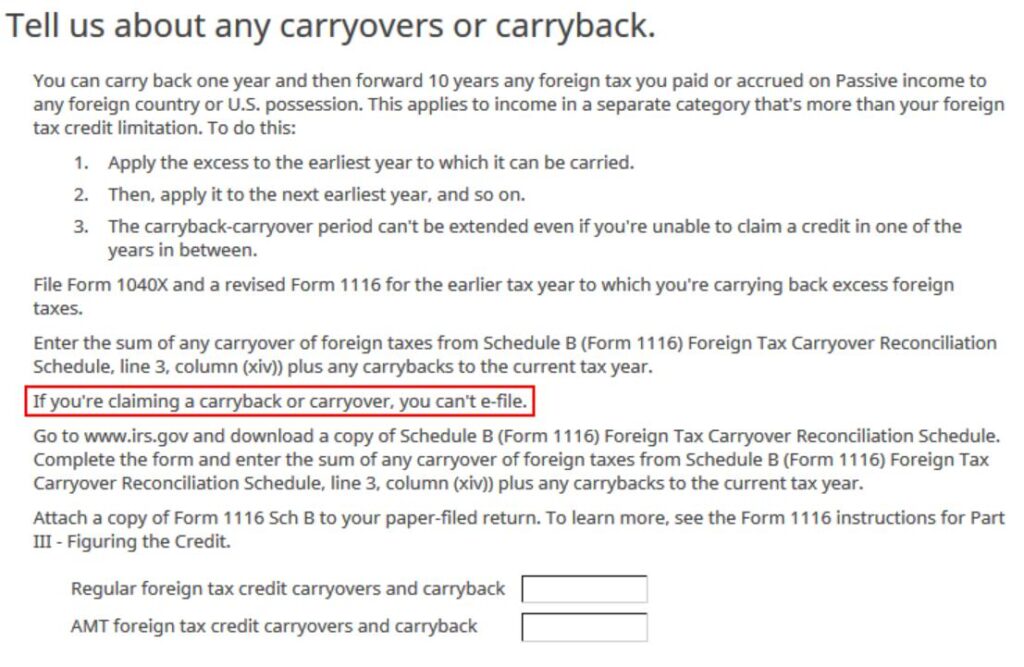

Fortunately, we don’t have any carryover or carryback. If we can’t get 100% credit for the foreign taxes paid this year, we’ll have to create a carryback or carryover, which means we can’t e-file with H&R Block.

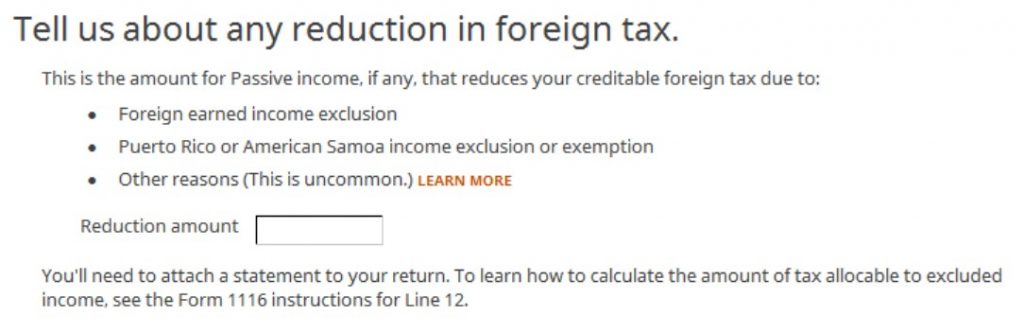

We don’t have any reduction either.

We don’t know what the foreign tax rate was. We’re leaving this blank.

We don’t know how to adjust. We’re leaving it blank again.

This is getting ridiculous. All I want is to get the foreign tax credit!

We’re finally done with Form 1116. Are we getting the credit?

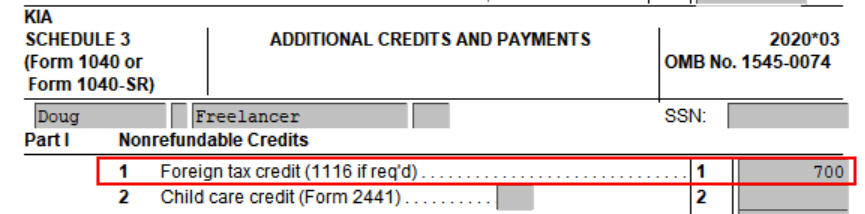

Verify on Schedule 3

Click on Forms on the top. Double-click on Form 1040 and Schedules 1-3.

Scroll down to Schedule 3. Line 1 shows our foreign tax credit. You can also look at Form 1116. It looks awfully complicated.

Excess Foreign Tax Credit

We received 100% of the foreign taxes paid as a tax credit in our example. If you paid higher foreign taxes on a lower US income, you may not be able to take 100% of the credit. You’ll have to wait until next year to take the rest of it.

Carrying over part of the credit to the following year requires filing a Form 1116 Schedule B. H&R Block doesn’t have this form in their program. H&R Block tells you to download the form from the IRS website, complete it yourself, and attach it to your paper return. That’s ridiculous.

Summary

H&R Block software works when you paid more in foreign taxes than the $300/$600 threshold that requires a Form 1116. You’ll have to gather the foreign income and the foreign dividends from the 1099 supplemental information from your brokers. After it’s all said and done, you’re getting a tax credit for taxes you paid to foreign countries through your mutual funds and/or ETFs.

H&R Block asks you to add up the foreign tax numbers yourself. It asks you to make any necessary adjustments to the foreign-source income, which is quite difficult. The option to activate the adjustment exception is hidden in the Forms mode. You’re on your own when you don’t qualify for the adjustment exception. It also asks you to handle any carryover yourself.

TurboTax does a better job of handling the foreign tax credit than the H&R Block software. See Foreign Tax Credit Form 1116 in TurboTax.

It’s better to avoid the complicated Form 1116 altogether next year by putting your international mutual funds and ETFs in a tax-advantaged account. See Too Much Hassle in Claiming Foreign Tax Credit on IRS Form 1116.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

{kind=link}