Fidelity Investments is best known as an administrator for workplace retirement plans and an online broker for retail investors. In addition to 401k/403b accounts, Traditional and Roth IRAs, HSAs, and taxable brokerage accounts, Fidelity also offers accounts that can be used for the same purpose as a checking account and a savings account.

Because Fidelity is interested in having a full relationship with its customers for both banking and investing and its primary focus is on the investing part, it’s in a good position to offer better rates and features than other banks in the banking part.

Here are three ways to use a Fidelity account to manage day-to-day spending and savings.

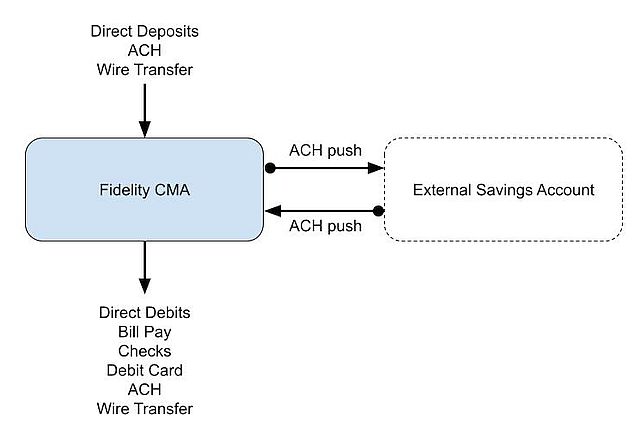

CMA as Checking

Fidelity Cash Management Account (CMA) is a separate account type from Fidelity’s regular taxable brokerage account officially called “The Fidelity Account.” You have to choose the account type when you open the account. A Cash Management Account can’t be changed to a regular taxable brokerage account after you open the account. Nor can an existing regular taxable brokerage account be changed to a CMA.

Included Features

The Cash Management Account is specifically designed to meet banking needs. It has pretty much everything people need for a checking account and nearly everything is free.

– FDIC-insured balance

– Pays interest (2.6% APY as of July 31, 2023)

– No minimum balance

– No monthly maintenance fee

– Does not require direct deposit

– Provides a routing number and an account number for direct deposits and direct debits

– Accepts check deposits by mobile app or dropoff at a Fidelity branch

– Free checkbook

– Free Visa debit card for purchase, ATM withdrawal, and teller cash advance

– Reimburses ATM fee charged by any ATM worldwide

– Free Bill Pay service with eBill

– Free same-day ACH

– Free wire transfers

The 2.6% interest rate is lower than the rate on many high yield savings accounts but it’s a lot higher than the rate on most online checking accounts. For example, although Ally Bank pays 4% on its savings account as I’m writing this, its checking account pays only 0.25%. Most high yield savings accounts don’t have all the checking features such as check writing, debit card, and Bill Pay.

Routing Number and Account Number

You see the routing number and account number for direct deposits and direct debits when you click on the three dots next to the account name.

Limitations

Fidelity Cash Management Account has some limitations that aren’t a deal-breaker to me.

– Does not accept deposits of physical cash.

– Does not support Zelle (but it works with PayPal, Venmo, Cash App, Apple Pay, and Google Pay).

– Does not link instantly through Plaid.

– Does not offer cashier’s checks.

– Recurring outgoing transfers only support monthly and annual frequencies.

– 1% transaction fee on debit card purchases in foreign countries. This fee doesn’t apply to international ATM withdrawals.

– ACH pulls and check deposits are held for up to four business days. The money still earns interest. It’s just not available for withdrawal while on hold.

I’ve used Fidelity CMA for at least 15 years. It’s my primary checking account. I use my otherwise dormant Bank of America checking account on those rare occasions when I need to deposit physical cash, use Zelle, link instantly through Plaid, get a cashier’s check, or set up recurring transfers on an odd schedule. I don’t use a debit card for purchases.

The hold time on ACH pulls and check deposits will shrink over time for established accounts on smaller amounts. My ACH pulls and check deposits are usually available for withdrawal on the second business day. I do an ACH push from the other side when I need it to be available immediately. See ACH Push or Pull: The Right Way to Transfer Money.

When you use the Fidelity CMA as your checking account, you can link it to an existing high yield savings account as you normally do with a checking account. You earn much higher interest in the Fidelity CMA than in a typical checking account.

CMA as Checking/Savings Combo

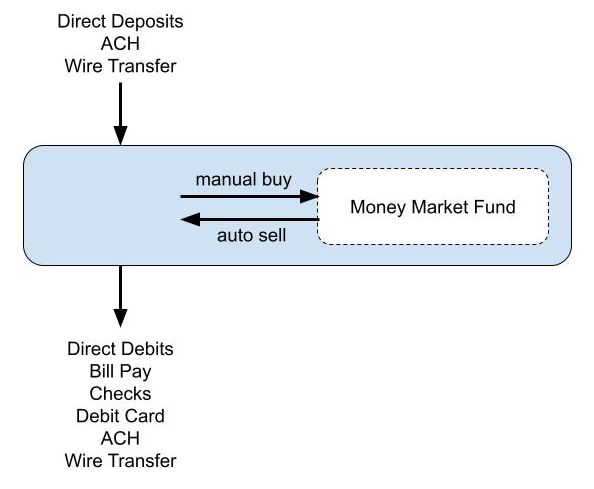

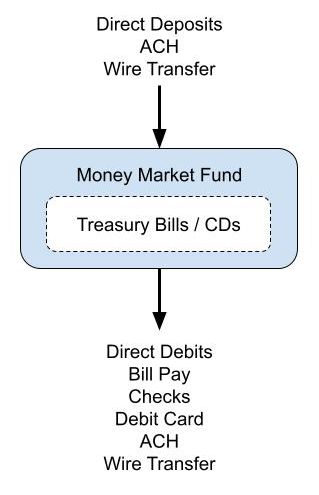

Instead of linking to an external savings account, you can buy a money market fund in the Cash Management Account and keep both checking and savings in the same account.

Buy Money Market Fund

Although the CMA is designed for banking needs, it’s still a brokerage account. With some exceptions (no margin or options), you can buy in the CMA pretty much everything that’s available in a regular brokerage account. That includes stocks, bonds, brokered CDs, mutual funds, and ETFs. A Fidelity money market fund pays about 4.8% annualized yield as of July 31, 2023, which is higher than the rate paid by many high yield savings accounts.

A money market fund isn’t FDIC-insured but when you buy a government or Treasury money market fund, the underlying investments in the money market fund are backed by the government. See No FDIC Insurance – Why a Brokerage Account Is Safe.

The CMA becomes a checking/savings combo when you buy a money market fund in it. The core balance in the CMA serves as the checking part and the money market fund serves as the savings part. You have to buy the money market fund manually but Fidelity will automatically sell from the money market fund when your core balance in the CMA is insufficient to cover a debit. This is like having free automatic overdraft transfers from savings to checking.

Because Fidelity will automatically sell from the money market fund to cover debits, if you’re so inclined, you can be aggressive in keeping the core balance in the CMA close to zero while keeping the bulk of your account in the money market fund earning a higher yield. Or you can set a maximum target balance alert with the Cash Manager to buy more shares of the money market fund when you have excess cash in the “checking” part.

Add Treasury Bills or Brokered CDs

If you’d like to take it one step further, you can also buy Treasury Bills or brokered CDs in the CMA when you have money that you know you won’t need for some time. The CMA then becomes a checking/savings/CD combo. The money automatically goes into the “checking” part when the Treasury Bill or brokered CD matures. For example, the amount set aside for the next property tax bill can go into a Treasury Bill or a brokered CD. See How To Buy Treasury Bills & Notes Without Fee at Online Brokers and How to Buy CDs in a Fidelity Brokerage Account.

Please note if you enable the “auto roll” feature when you buy new-issue Treasury Bills or brokered CDs in the CMA, the amount for the next roll reduces your “available to withdraw” number for a few days during the roll. A debit may fail if you don’t have enough available to withdraw. It’s not a problem if you don’t use auto roll or if you keep a substantially higher amount in cash and money market fund than the amount on auto roll.

I use a Fidelity Cash Management Account as a checking/savings/CD combo this way. I buy into the Fidelity Government Money Market Fund (FZCXX) when I have a large core balance. I also buy Treasury Bills with money I know I won’t need for some time. Fidelity automatically sells from the money market fund as needed to cover direct debits and outgoing transfers.

My setup works well but if I were to start from scratch, I would use a different setup below.

Separate Regular Brokerage Account

A regular Fidelity taxable brokerage account (“The Fidelity Account”) also provides a routing number and an account number for direct deposits and direct debits, free checks, debit cards, and Bill Pay. It includes basically everything in the CMA except ATM fee reimbursement but it uses a money market fund that pays a higher yield as the core position instead of the FDIC-insured balance as in the CMA.

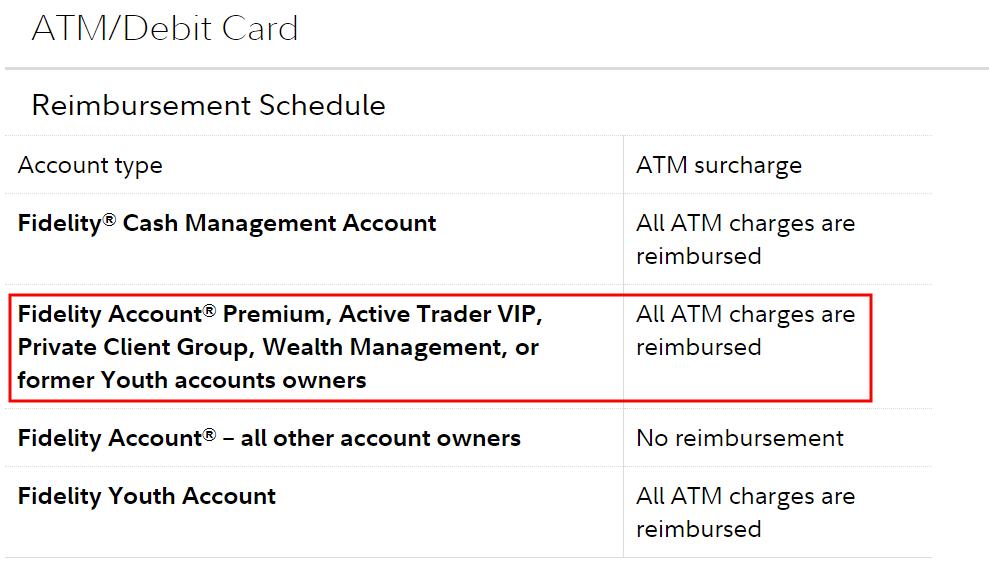

The ATM fee reimbursement is also included when you have Premium Services or Private Client Group status, which generally requires having $250k or more with Fidelity in all accounts. It doesn’t matter whether you have an assigned advisor.

You see your service level at the top right when you log in to Fidelity’s website. Contact customer service if you have more than $250k with Fidelity but you’re not given a premium service level.

Even if you don’t get ATM fee reimbursement, the higher yield on the core balance may very well cover the ATM fees several times over. Suppose your core position has an average balance of $3,000 during the year (the “checking” part in the CMA), a 2% higher yield pays $60 more in interest. That’s plenty to pay for ATM fees unless you frequently take ATM withdrawals. My account records show that I used an ATM only once in seven months so far this year.

| CMA | Regular Brokerage Account | |

|---|---|---|

| Core Position | FDIC insured | government money market fund |

| Yield on core position (as of July 31, 2023) |

2.6% | 4.8% |

| ATM fee reimbursement | included | included for some accounts |

The same missing features and limitations of the CMA also apply to the regular taxable brokerage account — no physical cash deposits, no Zelle, no cashier’s check, no instant Plaid, 1% foreign transaction fee on debit card purchases, and hold on ACH pulls and check deposits for up to four business days.

Set and Forget

Using a regular brokerage account for spending and savings becomes truly set-and-forget. You don’t have to manually buy a money market fund. All deposits automatically go into a money market fund that pays about a 4.8% yield as of July 31, 2023. All debits come out of this money market fund. It’s like using a savings account as a checking account.

You can still buy Treasury Bills or brokered CDs to set aside money for specific bills in the future. The same caveat on “auto roll” and “available to withdraw” as mentioned above also applies.

Name Your Accounts

Although you can keep the money for spending and short-term reserves in the same regular taxable brokerage account that also holds your long-term investments, most people probably prefer to keep them separate. You can have two (or more) regular taxable brokerage accounts for different purposes. You just give them different names to know which is which.

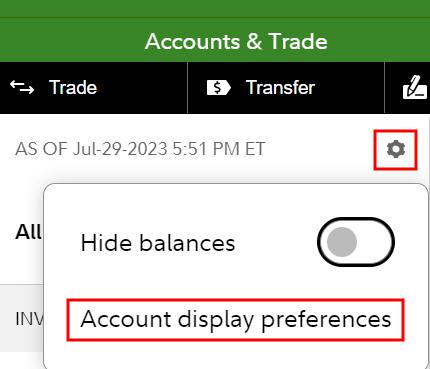

To change the display name of your accounts, click on the setup icon near the top left and then click on “Account display preferences.”

Check the box next to the account you’d like to name and then click on the “Rename” link on the top. Change the name to “Spending Account” or something to that effect.

You can also move an account to a different group to help you organize. There’s a built-in “Spend & Save Accounts” group but I leave my account in the “Investment Accounts” group so that it shows up on the top.

***

The biggest draw of using a Fidelity brokerage account for spending and short-term reserves is the checking features. You effectively use a savings account as a checking account and earn a good yield from the first dollar. Everything is seamlessly together.

A Vanguard money market fund and some less well-known high yield savings accounts pay more but when you pair it with a checking account that pays close to zero, the blended yield on all your cash goes down. You also have to manage the balance of your checking account and transfer money back and forth.

Transitioning a checking account takes some time and effort. Banks know it. That’s why they pay you close to zero on checking accounts. They bet that you think it’s too much trouble to switch. Don’t fall for it. It’s easier than you think when you take your time to make the move.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

![[Infographic] Main Processes For Purifying Water](https://blog.berichh.com/wp-content/uploads/2023/02/Infographic-120x86.png)

{kind=link}