Despite a long list of things that Fidelity’s retirement planning tool doesn’t do, I still use it as a high-level model. The planning exercise I did at the end of last year revealed two fundamental drivers of financial success in retirement.

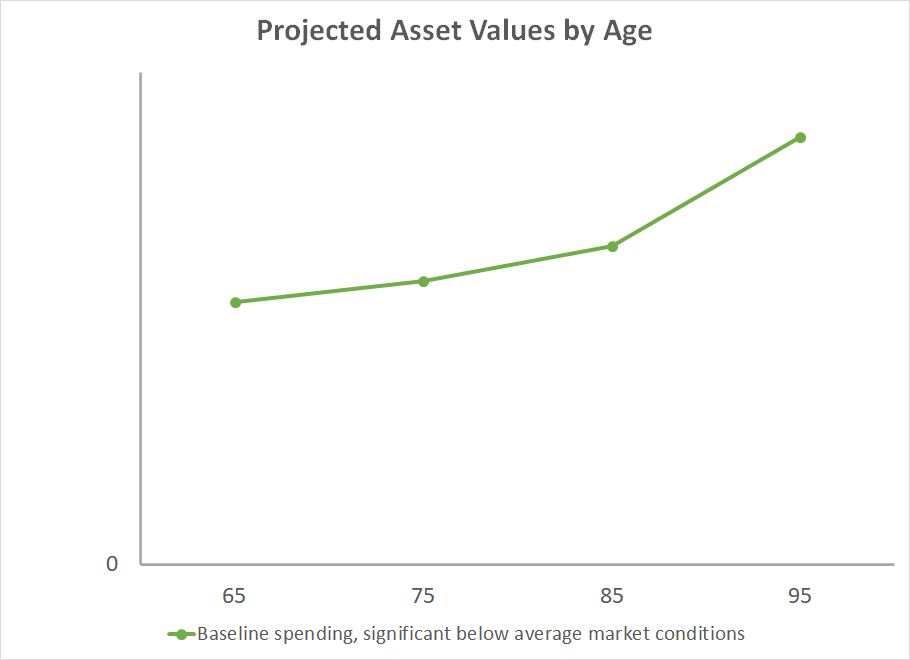

Baseline Spending

First, I created a baseline annual spending. The planning tool showed a table of the projected values of our investments at different ages when the investment returns are “significantly below average.” Significantly below average means “a scenario in which your outcome was successful 90% of the time” using historical data. I created this chart by sampling a few age milestones from the table:

All values are in today’s dollars. I’m not showing numbers on the vertical axis for obvious reasons.

Our investment portfolio is projected to increase while we take withdrawals to support the planned annual spending. That’s both good and bad. It’s good because it shows we have enough for our retirement. It’s bad because we don’t need or want 60% more money at age 95 than at age 65.

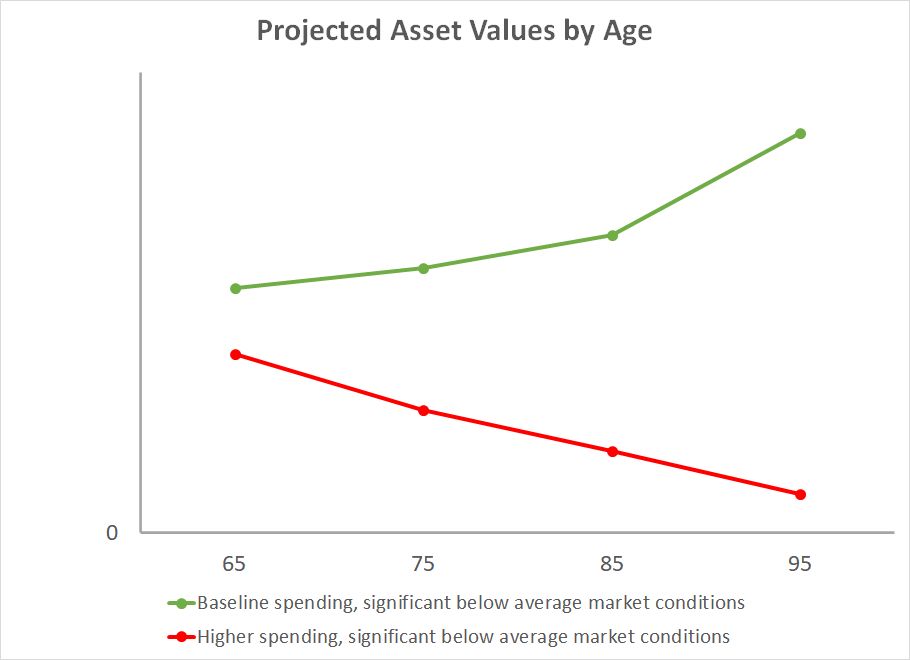

Higher Spending

Next, I increased the annual spending by 20%. The planning tool showed a different set of projected values:

Now the projected values go down with age. It gets dangerously close to zero at age 95. This means that our sustainable spending is somewhere between these two levels. If the future market returns are below 90% of returns in the past, we can still spend a little more than the baseline plan but not 20% more.

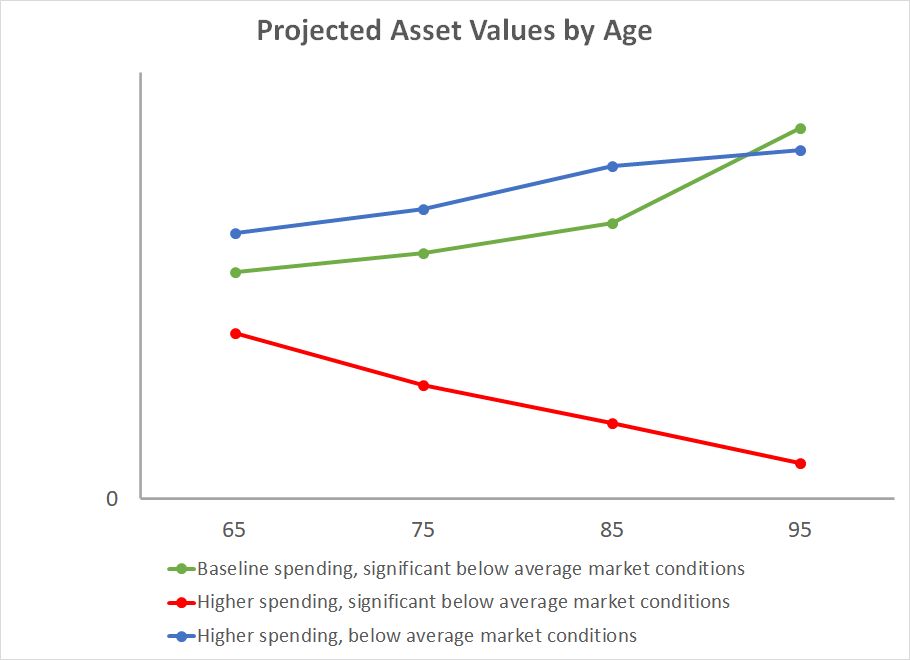

Better Market Conditions

The planning tool also produced a table of projected values for returns merely below average but not significantly below average. Below average means “a scenario in which your outcome was successful 75% of the time” as opposed to 90%. The projected asset values under these better market conditions while supporting the higher spending looks like the blue line in this chart:

It shows that if the returns are only below average — not significantly below average — our assets would be higher than the baseline scenario through age 90 while supporting 20% higher spending every year.

Fundamental Drivers

When I presented these three scenarios to my wife, she pointed out that it was only too obvious.

“You didn’t have to run a fancy tool to tell me that higher spending will drain our investments faster and better returns will help.”

She told me the same thing when I said I discovered the secrets to a fat 401k 11 years ago.

It’s obvious because it’s true. Spending and investment returns are indeed the two fundamental drivers of financial success in retirement because they compound. We can handle low returns (the green line) or higher spending (the blue line) but not both year after year if we live long (the red line).

When we think of the usual consternations in retirement planning — when to claim Social Security, which accounts to withdraw from first, when and how much to convert to Roth, buckets strategy or proportional withdrawals, buy an annuity or not, … — everything added together can’t alter our retirement trajectory as much as our annual spending and investment returns.

If we’re on the red line because our annual spending is too high relative to the investment returns, the most optimal tactics in Social Security claiming, Roth conversion, and withdrawal sequencing won’t yank us back to the green line. We’ll need to reduce spending. If we’re on the blue line because we aren’t so unlucky with investment returns, we’ll do just fine even if we aren’t so clever in retirement planning tactics.

You don’t have to use Fidelity’s retirement planning tool to see this effect. Any other tool will show the same two fundamental drivers.

Make It Robust

Retirement planning tactics are useful but we should make our plan NOT rely on them. If optimal executions of Social Security claiming, Roth conversion, and withdrawal sequencing make or break our retirement, it means our plan is too fragile. It isn’t robust enough when a slip in execution, a miscalculation, or a change of laws will knock us off track.

The goal should be to make our retirement successful regardless. When we get our spending right for the market conditions, any optimization tactics will only be icing on the cake, and suboptimal executions won’t jeopardize our retirement. If we get our spending wrong for the market conditions, no amount of optimization will rescue our retirement.

***

We’ll be watching the trajectory of our investments. If we see we’re at risk of going on the red line when we have a combination of high spending and low returns, we’ll reduce spending and try to move toward the green line. If we see that the market returns aren’t too bad, we’ll know we have more leeway in our spending. That’s how we’ll keep our eyes on the two fundamental drivers of financial success in retirement.

I told my wife that’s all she needs to do if something happens to me. Everything else is optional. How does SECURE Act 2.0 alter the financial success of our retirement? It does not, because it doesn’t change the two fundamental drivers.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

{kind=link}